Vancouver commercial real estate market update – Q1 2026

Vancouver reported a contraction in overall investment activity, with about $1.9 billion in dollar volume transacted, representing a 14% decrease year-over-year.

Vancouver commercial real estate market update – Q1 2026

Vancouver reported a contraction in overall investment activity, with about $1.9 billion in dollar volume transacted, representing a 14% decrease year-over-year.

Authors

Jennifer Nhieu

Senior Research Analyst

Arthur Tang

Senior Market Analyst

Key highlights:

Source: Altus data

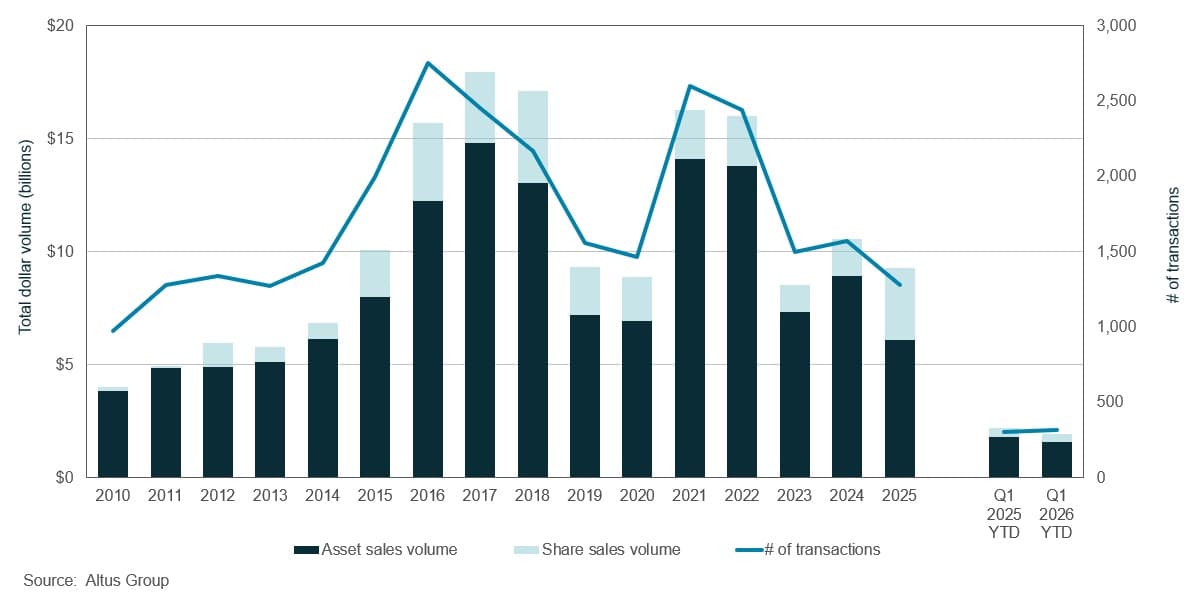

In the first quarter of 2026, Vancouver reported a contraction in overall investment activity, with about $1.9 billion in dollar volume transacted, representing a 14% decrease year-over-year

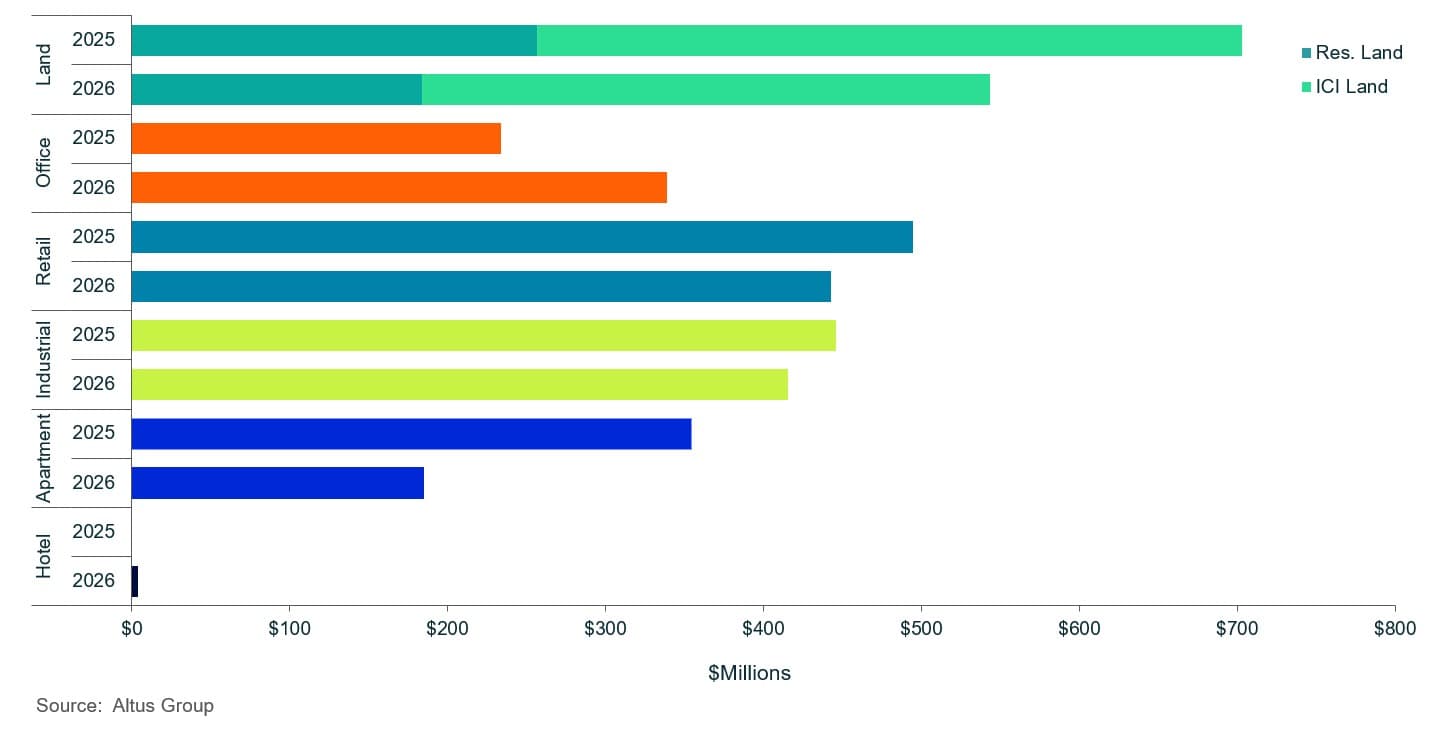

The office sector was the only core sector to report year-over-year growth, with a 45% increase in investment volume, recording $338 million in dollar volume transacted, while the multi-family sector experienced the most significant slowdown, recording $185 million in dollar volume transacted, representing a 48% year-over-year decrease

Forward-looking investor sentiment is defined by a disciplined, defensive commitment to capital preservation, where the pursuit of speculative development upside has been replaced by a demand for immediate, secure cash flow

Commercial investment in Vancouver experienced a contraction, down 14% year-over-year

Based on analysis of Altus data, during the first quarter of 2026, Vancouver’s commercial real estate market recorded a 14% year-over-year contraction in total investment volume to $1.9 billion, driven by a broad deceleration across most core asset classes, with the exception of office. This downward adjustment reflected a defensive yet highly calculated outlook among investors navigating an intricate macroeconomic landscape. While the Canadian economy successfully avoided a technical recession in 2025, economic growth remained weak, prompting capital to prioritize resilience over expansion. Market performance throughout the quarter was heavily influenced by lingering structural friction, including shifting regional population dynamics, escalated trade tensions with the United States and a broader softening of domestic consumer demand.

Figure 1: Vancouver property transactions - All sectors by year

Domestic monetary policy provided a baseline of stability through early 2026, anchoring long-term interest rate expectations. The Bank of Canada (BoC) maintained its target for the overnight lending rate, extending consecutive rate holds to combat persistent inflationary pressures. Regionally, this cooling manifested in the labour market. Data from Statistics Canada indicated that British Columbia’s unemployment rate rose to 6.7% by March 2026, with the Metro Vancouver region directly mirroring this 6.7% level. Concurrently, provincial economic output slowed, with British Columbia’s year-over-year GDP growth tracking at a modest 0.9% for the quarter.

In response to these conditions, investor sentiment in Vancouver shifted decisively toward capital preservation. Private and institutional capital bypassed speculative land and high-risk development opportunities, focusing almost exclusively on defensive asset classes backed by secure, stabilized cash flows. Ultimately, the first quarter marked a transition toward highly calculated asset underwriting as market stakeholders adjusted to the operational realities of a prolonged neutral interest rate environment.

Vancouver office real estate investment activity

The office sector recorded a transaction volume of $338 million, a 45% increase year-over-year. This increase underscored a persistent confidence in Vancouver’s stabilizing office market. According to Altus Group’s latest Canadian Office Market Update, Vancouver’s office availability rate reached 12.8%, representing a 50 basis point (bps) increase year-over-year. This figure remained stubbornly elevated, having stabilized in the 12%-13% range for three consecutive years due to persistent hybrid work trends and cautious corporate downsizing.

An enduring characteristic of the office market was the bifurcation of leasing activity. Investors and occupiers exhibited a distinct “flight-to-quality,” favouring premium, amenitized Class-AAA spaces in transit-oriented hubs. While these top-tier assets maintained relatively tight vacancy rates and elevated rents, older Class B and C properties faced increasing downward pressure as tenants prioritized modern workplace environments to meet return-to-office mandates. Based on Altus Data Studio data, leasing activity in the first quarter of 2026 corroborated this preference for premium assets.

Class A transactions constituted the majority of the activity, accounting for 42 deals, encompassing nearly 859,000 square feet.

Conversely, Class B office space saw considerably less demand, comprising only three transactions, which totalled approximately 79,000 square feet

On the development front, the first quarter saw the completion of one fully leased office building, 5670 Cambie Street, totalling 21,000 square feet. Regarding the future pipeline, Vancouver has eight office buildings under construction, totalling nearly 910,000 square feet, with 34% of the space available for lease. The limited development pipeline moving forward will be a critical factor in the anticipated near-term tightening of availability rates, as less new supply will come online to compete with existing inventory.

Vancouver retail real estate investment activity

In the first quarter of 2026, the retail sector entered a highly bifurcated, selective phase, with nearly $443 million in dollar volume transacted, a 10% decrease. While core retail fundamentals exhibited early signs of stabilization, buoyed by increased population density and transit expansion, the legacy of recent economic headwinds remained visible. Restructuring among large-format department stores and big-box contractions introduced large blocks of space into the retail market. However, availability within urban formats and food-anchored retail remained exceptionally tight.

As corporate expansion strategies turned ultra-selective, high-density urban corridors continued to attract luxury flagships, alongside convenience-driven, service-based banners that catered to cost-conscious consumer behaviour. Concurrently, new supply remained highly constrained due to elevated construction costs and restrictive near-term financing, ensuring that new development was strictly disciplined and heavily indexed toward mixed-use formats and suburban asset intensification.

Within the capital markets, investor sentiment was active but deeply risk-averse. Persistent inflation risk factors triggered a tightening bias from the BoC, which dampened expectations for lower borrowing costs and prompted capital to adopt a defensive posture. Consequently, investors demonstrated a clear preference for well-leased, grocery-anchored or necessity-based assets that offered immediate, secure cash flow. Despite this macroeconomic friction, confidence in premier locations remained robust. The market continued to command an immense pricing premium for downtown street frontages, as highlighted by the high-profile sale of 1101, 1121 & 1133 Alberni Street.

Vancouver industrial real estate investment activity

During the first quarter of 2026, the industrial sector demonstrated resilience, with core fundamentals stabilizing as the market actively digested a recent wave of completions. Acute geographic constraints and a structural scarcity of industrial land have long limited inventory expansion; the market has historically maintained positive net absorption. While a temporary supply-demand imbalance briefly softened conditions in early 2025, the first quarter of 2026 recorded a strong return to positive territory with nearly 722,000 square feet of net absorption. According to Altus Group’s latest Canadian Industrial Market Update, Vancouver’s availability rate stood at 6.0%, representing a modest 10 basis point year-over-year increase, signalling that tenant demand remained fundamentally well-aligned with existing inventory.

This stabilization was further reinforced by a disciplined contraction in the development pipeline, as stakeholders reacted to shifting macroeconomic indicators. The active construction pipeline fell to 25 industrial buildings totalling nearly 1.4 million square feet, with approximately 65% of the space remaining available for lease. This reduction reflected a strategic pull-back by developers, who increasingly bypassed speculative projects in favour of strict pre-leasing requirements to mitigate elevated construction and financing costs. Concurrently, this cautious climate extended to the capital markets, where first-quarter industrial investment volume totalled $415 million, marking a 7% decrease year-over-year.

Leasing conditions were characterized by a distinct structural bifurcation rather than a broad decline across the various segments. Modern high-specification functional logistics continued to command premium rents due to persistent demand. Within the small to mid bay segments, newer assets saw robust demand owing to their operational flexibility for diverse tenants. However, because a notable percentage of this small to mid bay inventory consisted of older legacy builds, these assets failed to align with modern tenant requirements, creating downward rental pressure and forcing property owners of these secondary properties to expand tenant inducements to sustain occupancy.

Vancouver multi-family real estate investment activity

Vancouver’s multi-family sector experienced a marked contraction in capital deployment, with total investment volume falling to $185 million, representing a sharp 48% year-over-year decline. This deceleration was primarily driven by a defensive shift in investor sentiment amid persistent macroeconomic pressures. Elevated borrowing costs continued to undermine the feasibility of new projects and shifted capitalization rate expectations, while a sudden surplus of unabsorbed condominium inventory and a pronounced decline in overall residential sales introduced additional friction. However, rather than remaining entirely sidelined, institutional capital selectively resurged to target core, newly completed purpose-built rental assets. This institutional appetite competed alongside private capital, with buyers prioritizing stabilized, transit-oriented assets that offered secure cash flows to mitigate macroeconomic friction and a softer residential sales market.

On the operational front, the market adjusted as an unprecedented wave of apartment completions met softening demand dynamics. A reduction in non-permanent residents, combined with heightened affordability constraints, slowed regional population growth and cooled the pace of rent appreciation. While the downtown core remained comparatively resilient, suburban submarkets experienced a more pronounced downward pressure. Rising vacancy rates and unabsorbed inventory across recently completed premium developments forced property owners to adapt, frequently relying on expanded tenant inducements and recent concessions to protect occupancy levels and recalibrate rental pricing across the metropolitan area.

Vancouver land real estate investment activity

The land sector, encompassing both residential land and ICI land segments, transitioned into a highly selective investment environment. Total transaction volume reflected a broader market stabilization effort, as buyers intentionally pivoted away from speculative plays with “development upside” in favour of assets providing income certainty. While macroeconomic headwinds and restrictive financing structures continued to temper overall deployment, capital allocation remained steady for properties featuring strong fundamentals or favourable transit zoning that provided long-term stability.

The residential land sub-sector recorded a decline in activity, heavily influenced by developers adjusting pipelines to manage elevated construction costs and prolonged municipal approval structures. This resulted in nearly $184 million in dollar volume transacted, representing a 28% year-over-year decrease. A notable strategic shift emerged during this period. Despite a generalized pause, urban rezoning activity remained highly resilient. This targeted momentum was particularly concentrated within major transit-oriented regions, such as the City of Vancouver’s Broadway Plan corridor, where developers selectively acquired and banked high-density multi-family parcels to leverage long-term provincial housing mandates.

Concurrently, the ICI land sub-sector continued to face structural friction, with $359 million in dollar volume transacted, representing a 20% year-over-year decline, as the bid-ask gap between vendor expectations and buyer underwriting remained stubbornly wide. While industrial and core commercial parcels benefited from underlying scarcity, many property owners remained anchored by historical peak valuations, creating a prolonged pricing disconnect. Consequently, transaction volume stayed constrained as investors backed away from land that lacked immediate cash flow, unwilling to pay the high ongoing costs of holding an inactive asset. This persistent gap forced a strategic pause on ICI land acquisitions, directing capital instead toward the optimization and build-out of existing core holdings where project feasibility was already established.

Figure 2: Vancouver property transactions by asset class year-to-date

Notable Vancouver commercial real estate transactions

The following are the notable transactions for the Q1 2026 Vancouver commercial real estate market update:

1101, 1121 & 1133 Alberni Street – Retail

In early March 2026, three luxury retail units within the Hyatt Vancouver Downtown Alberni (Formerly Shanri-La Vancouver) retail podium traded for $55 million from Brookfield Asset Management to Aquilini Investment Group. The units totalled 40,996 square feet and reflected approximately $1,342 per square foot.

This transaction followed Brookfield Asset Management’s June 2025 acquisition of the 15-storey hotel component and adjoining commercial podium of the Hyatt Vancouver Downtown Alberni from Westbank Corp. and Peterson Group via share sale, for a total of $160 million.

The retail units were fully leased to a strong roster of national and international tenants, including Burberry, Urban Fare and The Keg, providing stable in-place income supported by a long weighted average lease term. The sale included 79 parking stalls and offered future rental growth potential through lease rollovers and market rent reset opportunities.

17650 66A Avenue, Surrey – Office

Industra Holdings Ltd. acquired a three-storey, 15,640 square foot office building at 17650 66A Avenue in Surrey from Mitchell Group Investments Inc. for $11.8 million, which reflected approximately $754 per square foot. Constructed in 2009 by Mitchell Group, the transaction closed in late March 2026 and marked the establishment of Industra’s new corporate head office in Metro Vancouver.

Situated within Surrey’s Cloverdale neighbourhood, the property benefited from convenient access to Highway 15, Highway 10, Fraser Highway, and the broader Metro Vancouver transportation network. The area has experienced significant residential and commercial growth in recent years, attracting a range of professional, industrial, and service-sector businesses seeking a presence in one of British Columbia’s fastest-growing municipalities, making it well-suited for a corporate headquarters operation.

1710 East Pender Street, Vancouver – Residential Land

Alt Commercial Housing Society acquired a 0.596-acre high-density development site from Lu’ma Native Housing Society for $13.0 million, which reflected approximately $87 per buildable square foot. The transaction closed on February 26, 2026.

Located in the Grandview-Woodland neighbourhood, with strong access to Downtown Vancouver and the Broadway corridor. The site was approved for the “Place of Cedars” project, an 18-storey, 191-unit Indigenous-led social housing development with approximately 149,801 square feet of buildable area.

The acquisition supported ongoing demand for redevelopment sites from non-profit housing providers. Vancouver City Council also approved up to $12.3 million in CHIP funding in February 2026 to support construction.

5085 North Fraser Way, Burnaby – Industrial

Groupe Montoni acquired the 106,100 square foot multi-tenant industrial property at 5085 North Fraser Way for $53.27 million, or approximately $502 per square foot. The transaction closed on March 23, 2026. The asset, located in Burnaby’s Big Bend industrial area, was occupied by Dorigo Systems and Oxygen8. The deal included a sale-leaseback with Dorigo, while Oxygen8 entered into a long-term lease for approximately 55,000 square feet for its headquarters and production facility.

The property is located within Burnaby’s Big Bend industrial area, one of Metro Vancouver’s most established industrial nodes, offering strong connectivity to major transportation corridors including Marine Way, Highway 91, Highway 99, and the Trans-Canada Highway. The acquisition highlighted continued investor demand for well-located industrial assets with stable tenancy in Metro Vancouver’s supply-constrained market.

Crestwood, 11300 Pazarena Place, Maple Ridge – Apartment

Anthem Properties acquired Crestwood, a 24-unit mixed-use rental and daycare property from Polygon Homes, for $17.25 million, reflecting approximately $718,750 per residential unit.

Located near Lougheed Highway within the Provenance community, the three-storey building, completed in 2024, included 18,491 sq ft of residential space above a fully leased 7,173 square foot daycare with an outdoor play area. The asset represented a newly completed, institutionally designed mixed-use rental project in the Maple Ridge residential market.

The acquisition reflected continued investor demand for newly built, stabilized rental housing assets in suburban Metro Vancouver communities, particularly those with integrated community amenities and strong tenant demand fundamentals.

Vancouver commercial real estate market outlook

Moving into the remainder of 2026, the Vancouver commercial real estate market is adjusting to a clear shift in investor mindset, moving away from the high volatility of recent years toward a period of highly cautious and careful property evaluation. With capital markets operating under a continuous BoC rate hold and ongoing energy-driven inflation risks, previous expectations for interest rate relief have officially reset. Consequently, forward-looking investor sentiment is defined by a disciplined, defensive commitment to capital preservation, where the pursuit of speculative development upside has been replaced by a demand for immediate, secure cash flow.

This cautious approach is widening a distinct performance and pricing gap across the market. Institutional and private buyers are focusing heavily on core, high-density urban locations and necessity-based properties that offer proven protection against broader economic challenges. On the other hand, older or poorly located buildings that fail to meet modern business needs face a slower sales process and downward price adjustments. As stakeholders navigate back-to-back quarters of flat national economic growth, investment activity is expected to remain steady, but highly selective, keeping the near-term focus squarely on asset resilience, operational flight-to-quality, and defensive income security.

Want to be notified of our new and relevant CRE content, articles and events?

Disclaimer

This publication has been prepared for general guidance on matters of interest only and does not constitute professional advice or services of Altus Group, its affiliates and its related entities (collectively “Altus Group”). You should not act upon the information contained in this publication without obtaining specific professional advice.

A number of factors may influence the performance of the commercial real estate market, including regulatory conditions and economic factors such as interest rate fluctuations, inflation, changing investor sentiment, and shifts in tenant demand or occupancy trends. We strongly recommend that you consult with a qualified professional to assess how these and other market dynamics may impact your investment strategy, underwriting assumptions, asset valuations, and overall portfolio performance.

No representation or warranty (express or implied) is given as to the accuracy, completeness or reliability of the information contained in this publication, or the suitability of the information for a particular purpose. To the extent permitted by law, Altus Group does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. The distribution of this publication to you does not create, extend or revive a client relationship between Altus Group and you or any other person or entity. This publication, or any part thereof, may not be reproduced or distributed in any form for any purpose without the express written consent of Altus Group.

Authors

Jennifer Nhieu

Senior Research Analyst

Arthur Tang

Senior Market Analyst

Resources

Latest insights