US CRE operating fundamentals hold steady to start 2026

Private market performance remains resilient, with sector-level divergence pointing to selective opportunities for long-term investors.

Key highlights

Alex Jaffe and Mike Amthor from Altus Group's Valuation Advisory practice sat down with Altus Group's Research Team on a recent episode of the CRE Exchange podcast to discuss Q1 2026 NCREIF ODCE results, building on their quarterly performance webinar

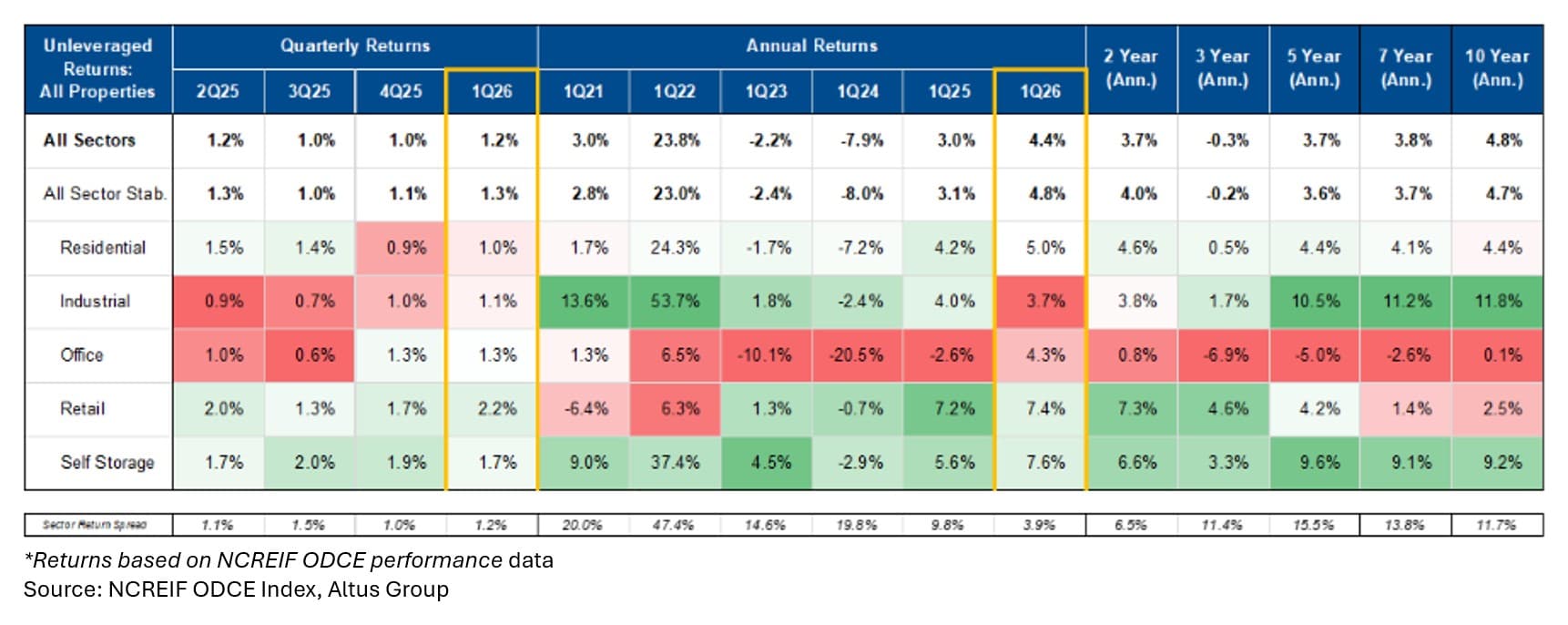

The NCREIF ODCE Index posted a 1.2% unlevered total return in Q1 2026, continuing a pattern of muted but stable performance

Retail led all major sectors at 2.2%, while office, industrial, and residential clustered between 1.0% and 1.3%

Industrial weakness remains concentrated in Southern California, now three years into a correction, while a recovery is emerging in markets like Atlanta, Chicago, and Dallas

Gateway residential markets outperformed as Sunbelt supply pressures continued, while self-storage posted steady gains and office showed early signs of leasing-driven stabilization in select markets

Retail fundamentals continue to outperform expectations, though consumer spending resilience remains the key watch item heading into the second half of the year

Alex Jaffe and Mike Amthor from Altus Group's Valuation Advisory practice recently joined the Research Team on the CRE Exchange podcast to unpack Q1 2026 NCREIF ODCE results. Jaffe and Amthor had covered the data in depth in their quarterly performance webinar, and the podcast gave the Research Team an opportunity to dig into the findings and add broader context from publicly traded REIT earnings calls, which largely echoed the findings of the ODCE data. Below are the Research Team's key takeaways from the conversation.

The NCREIF ODCE Index returned 1.2% on an unlevered property basis in the first quarter, driven primarily by income with light positive appreciation and yields more or less unchanged. One data point that stood out: capital expenditure at the property level came in notably lighter than in recent periods. "There are really two ways of looking at that," says Jaffe. "The optimistic way is that landlords have spent the past two or three years investing in their properties, and because we're seeing those capital numbers lighter in the current quarter, we are hopeful that future leasing will be better." The less optimistic read is that some owners are deferring necessary maintenance.

Figure 1: ODCE Index total return by sector

Gateway markets reclaim the lead in residential real estate

Gateway markets, including San Francisco, Chicago, and New York, led the residential sector with positive appreciation, while Sunbelt markets, including Dallas, Raleigh, Denver, San Diego, and Orlando, saw values decline. "The story in each of those is rents," says Amthor. "Strengthening rents in those gateway markets, weakening rents in the Sunbelt markets, and that's really an inversion of what we had seen earlier in this post-pandemic cycle." San Francisco is a particular standout, with AI industry employment generating strong rental demand against very limited new supply.

SoCal industrial real estate correction continues, recovery emerges elsewhere

Southern California's industrial correction is now in its third year, with pure warehouse rents in the Inland Empire falling a further 2% in the first quarter. Miami and New York also showed signs of slowing. The recovery story is emerging elsewhere, with Atlanta, Chicago, Houston, Dallas, and Phoenix all showing positive appreciation, supported by a national construction pipeline now at 1.7% of total stock, well below the 10-year average of 2.6%.

Investor interest in Southern California is beginning to return at two ends of the size spectrum. "We're seeing gravitation towards larger spaces, 500,000 square feet or greater, with longer-term warehouse leases," says Jaffe, "and at the other end, a number of funds are looking at smaller industrial spaces under 100,000 square feet, where operators can renovate suites, attract stronger tenants, and reset rents."

Office real estate performance remains an asset-specific story

Office returned 1.3% in Q1, though appreciation remains negative in aggregate. Pockets of positive returns emerged in San Francisco, New York, Dallas, Houston, and Los Angeles. "It's as if the market is differentiating, as it should, the winners and losers from where tenants want to locate," says Jaffe. "We're seeing this in the same submarkets, but it's a block away from each other." That divergence is also showing up across fund portfolios, generating active conversation around vintage and whether capital allocated in 2021 and 2022 would be deployed the same way today.

Retail real estate continues to surprise to the upside

Retail led all sectors at 2.2%, with mall, strip, and street all posting positive appreciation. Cash leasing spreads came in at double-digits across new and renewal leases, and same-store NOI growth was notably strong. "Each quarter, retail continues to surprise us with strength in the cash flows," says Jaffe. The key watch item is the consumer, with a K-shaped dynamic becoming a recurring theme on REIT calls. So far, a meaningful pullback has not materialized.

Self-storage real estate posts steady gains as supply headwinds clear

Self-storage returned 1.7% in Q1, led by gateway markets and driven by improving cash flow fundamentals. The sector's repricing experience was less severe than most property types, and supply headwinds that weighed on performance for several years appear to be clearing. AI-driven automation and expense efficiencies are a growing topic in client conversations.

Looking ahead: entry points come into focus

The most consistent theme from both conversations was the tone around entry points. "If they're able to enter the market at an attractive point, 2026 and 2027 could be the right entry point as they think about their portfolios not just one year out, but three, five, or seven years out," says Jaffe. Despite ongoing uncertainty around rates, tariffs, and geopolitics, the private market has remained stable, and the conditions for patient, long-term capital to find opportunity are increasingly in place.

For a deeper dive into the Q1 2026 ODCE data, watch the full NCREIF ODCE quarterly performance webinar with Jaffe and Amthor, or listen to the full CRE Exchange episode.

This article draws on Altus Group's Q1 2026 NCREIF ODCE quarterly analysis, presented by Alex Jaffe, Senior Director, and Mike Amthor, Director, from Altus Group's Valuation Advisory practice, and discussed on the CRE Exchange podcast with Omar Eltorai, Senior Director of Research, and Cole Perry, Associate Director of Research. Additional context was drawn from publicly traded REIT earnings calls.

Want to be notified of our new and relevant CRE content, articles and events?

Boost investor confidence with independently managed valuations

Independent appraisals trusted by funds, investors, lenders, and public entities around the world.

Disclaimer

This publication has been prepared for general guidance on matters of interest only and does not constitute professional advice or services of Altus Group, its affiliates and its related entities (collectively “Altus Group”). You should not act upon the information contained in this publication without obtaining specific professional advice.

A number of factors may influence the performance of the commercial real estate market, including regulatory conditions and economic factors such as interest rate fluctuations, inflation, changing investor sentiment, and shifts in tenant demand or occupancy trends. We strongly recommend that you consult with a qualified professional to assess how these and other market dynamics may impact your investment strategy, underwriting assumptions, asset valuations, and overall portfolio performance.

No representation or warranty (express or implied) is given as to the accuracy, completeness or reliability of the information contained in this publication, or the suitability of the information for a particular purpose. To the extent permitted by law, Altus Group does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. The distribution of this publication to you does not create, extend or revive a client relationship between Altus Group and you or any other person or entity. This publication, or any part thereof, may not be reproduced or distributed in any form for any purpose without the express written consent of Altus Group.

Author

Cole Perry

Associate Director of Research, Altus Group

Author

Cole Perry

Associate Director of Research, Altus Group

Resources

Latest insights