Key highlights

The Greater Toronto Area (GTA) reported $22.8 billion in dollar volume for 2023; despite this slowdown, Toronto remains one of the top three preferred markets amongst investors, along with Vancouver and Ottawa

With the Bank of Canada (BoC) currently holding rates steady, a 2024 decrease in rates and a subsequent boost in investment activity is expected in the second half of the year

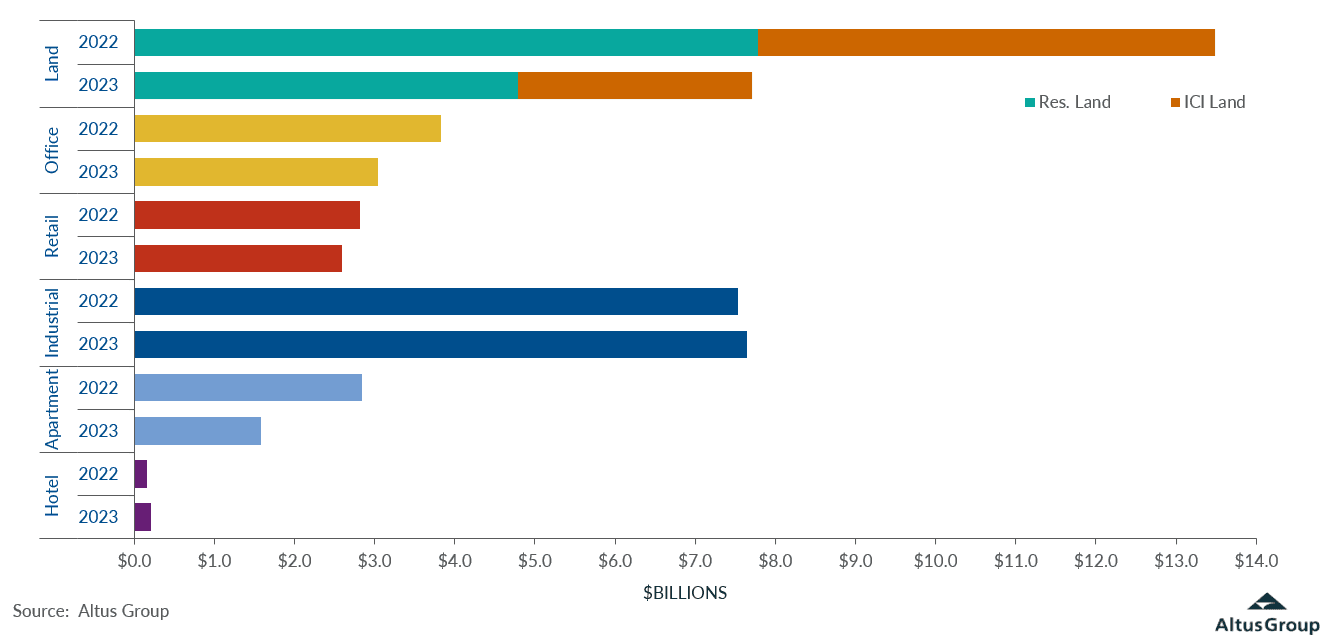

Investment activity in the industrial sector remained flat, reporting $7.6 billion in dollar volume transacted, a marginal increase year-over-year (YoY)

The office sector posted $3 billion in transactions, a 21% decrease YoY

The retail sector reported $2.6 billion in dollar volume transacted, an 8% decrease YoY

The multi-family sector recorded $1.6 billion in dollar volume transacted, a 44% decrease compared to 2022

The hotel sector has observed a gradual rebound in operations and investor sentiment, with $202 million in dollar volume transacted, representing a 24% increase YoY

Investment activity down in the Greater Toronto Area as higher interest rates and inflationary pressures introduced uncertainty

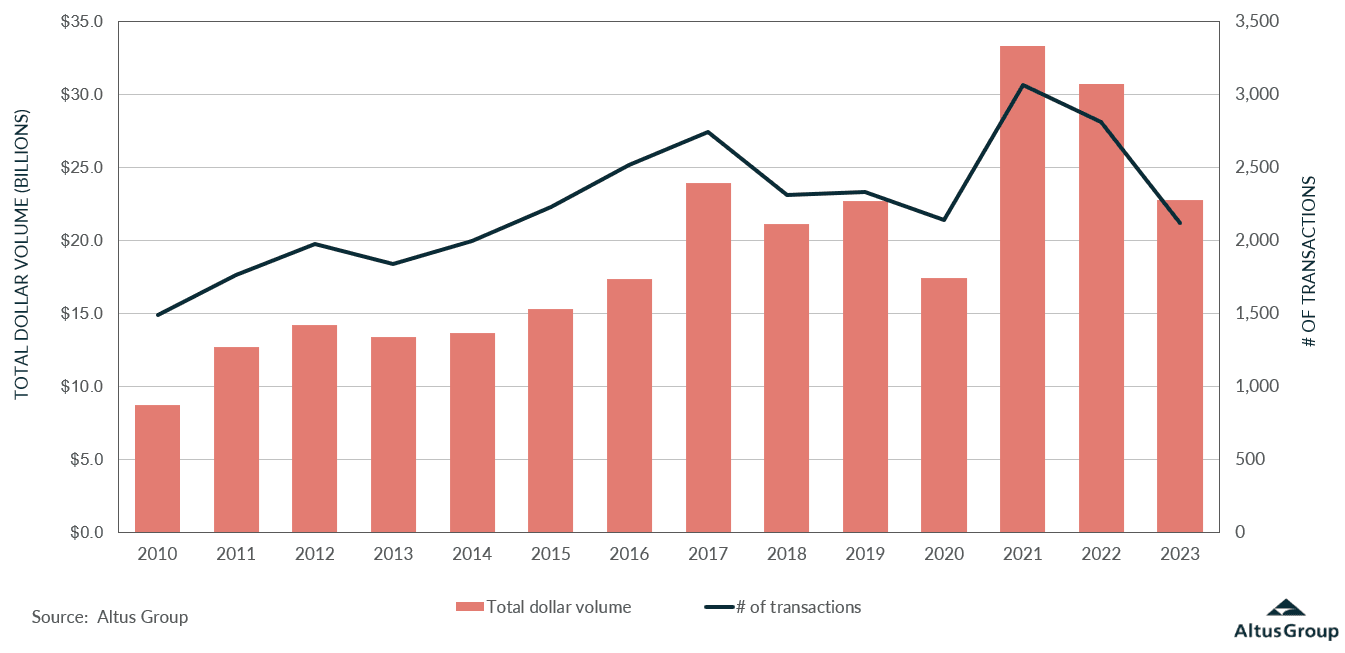

The Greater Toronto Area (GTA) reported $22.8 billion in dollar volume for 2023, down about 25% compared to 2022. Rising interest rates and inflationary pressures contributed to continued economic uncertainty and a slowing market as investors entered a price discovery phase. Tight lending practices from financial institutions in addition to a shortage of skilled labour, soaring construction and material costs, and price expectations between buyers and sellers further hampered market activity. Despite this slowdown, Altus Group’s most recent Investment Trends Survey identified Toronto as one of the top three preferred markets amongst investors, along with Vancouver and Ottawa. With the Bank of Canada (BoC) currently holding rates steady, a 2024 decrease in rates and a subsequent boost in investment activity is expected in the second half of the year. The caveat? If inflation and economic growth deviate from the Bank’s expectations, any rate decreases could be pushed further into the future.

Figure 1 - GTA property transactions – All sectors by year (Q4 2023)

Investment activity in the industrial sector remained flat, reporting $7.6 billion in dollar volume transacted, a marginal increase year-over-year (YoY). According to Altus Group’s most recent Canadian industrial market update, Toronto’s industrial availability rate increased by 0.8 percentage points to 3.4%. Moreover, the GTA saw a record-breaking quarter for industrial completions, adding 8.8 million square feet of new supply, with 33% pre-leased. In addition, 11.3 million square feet of new supply is currently under construction as the demand for modern industrial product persists.

While office space requirements have diminished, the GTA has observed a gradual return to office as more Canadians transitioned to the hybrid work model. The office sector posted $3 billion in transactions, a 21% decrease YoY. Altus Group’s latest Canadian office market update revealed that Toronto’s office availability rate has flattened to 18.1%. The market saw approximately 786,000 square feet of new supply in Q4 2023, with nearly one-third pre-leased. In addition, 6.1 million square feet of new supply is under construction, with over half pre-leased.

The retail sector reported $2.6 billion in dollar volume transacted, an 8% decrease YoY. Given the slowing economy and rising cost of living, Canadians have focused their expenditure on necessities. Furthermore, the hybrid work model has allowed Canadians to work, shop and play closer to home, and local neighbourhood retailers have reaped the benefits of increased foot traffic. Investors are adapting to these changes in consumer behaviour by investing in food-anchored retail strips, as these centres have demonstrated resilience to economic uncertainty and the impact of e-commerce.

The multi-family sector recorded $1.6 billion in dollar volume transacted, a 44% decrease compared to 2022. As aforementioned, difficulties securing financing and a multitude of challenges associated with the economic slowdown have contributed to sluggish investment activity. Regardless of the sector’s volatility, as markets across Canada continue to be plagued by an affordable housing crisis, the demand for purpose-built rentals remains high, and activity is expected to rebound with the anticipation of lower interest rates.

Residential and ICI land sales have both slowed, with $7 billion in dollar volume transacted, representing a 46% decrease YoY. The residential land market posted $4.1 billion, while ICI land posted $2.9 billion, a 44% decrease and a 49% decrease YoY, respectively. The decline in land investment can be attributed to difficulties securing financing in a high-interest-rate environment.

Notably, the hotel sector has observed a gradual rebound in operations and investor sentiment, with $202 million in dollar volume transacted, representing a 24% increase YoY. Investors have been strategic with their hotel investments as they look for opportunities in major urban markets supported by increased demand for lodging and the weaker dollar boosting the tourism industry.

Figure 2 - GTA property transactions by asset class (2022 vs. 2023)

Notable transactions for Q4 2023

Oxford – TPG Portfolio, Brampton & Vaughan – Industrial

Representing the largest industrial transaction of 2023, US-based TPG purchased a 75% stake in the Oxford-owned Brampton Business Park and Vaughan Business Park for $990 million, representing an aggregate adjusted price per square foot of $258. Oxford will continue to oversee the 5.1 million square foot portfolio and has kept a 25% stake in the properties. There are five buildings in each business park, with an approximate floor area of 2.2 million square feet in Vaughan and 2.9 million square feet in Brampton.

Vaughan Mills Shopping Centre, Vaughan – Retail

LaSalle Investment Management acquired a 49% stake in Vaughan Mills Shopping Centre from Ivanhoé Cambridge for $470.2 million. The transaction was part of a syndication process with both parties acting as co-owners and Ivanhoé Cambridge continuing to operate as asset managers. This represents the largest retail transaction of the year for the GTA. Containing a gross floor area of approximately 1.5 million square feet, the prominent shopping centre was purchased for an adjusted price per square foot of $640.

Langstaff Road East, Markham – Residential Land

Condor Properties acquired this site for $175.6 million from the Ontario Ministry of Infrastructure, representing the quarter's largest residential land transaction. The approximately 6.3-acre site is part of Markam's proposed Langstaff Gateway master plan community near Yonge Street and Highway 407.

320 McCowan Road, Scarborough – Residential Land

The subject property is improved with a 19-storey apartment building containing 300 units on a 4.2-acre site. Blauson Asset Management acquired the property for a total of $78 million, which consists of the assumption of mortgages and the issuance of an unsecured promissory note. The purchaser has submitted development applications to add two new residential towers of 25 and 29 storeys while maintaining the existing 19-story apartment building. The proposed new towers will contain 483 residential units and a gross floor area of 603,877 square feet.

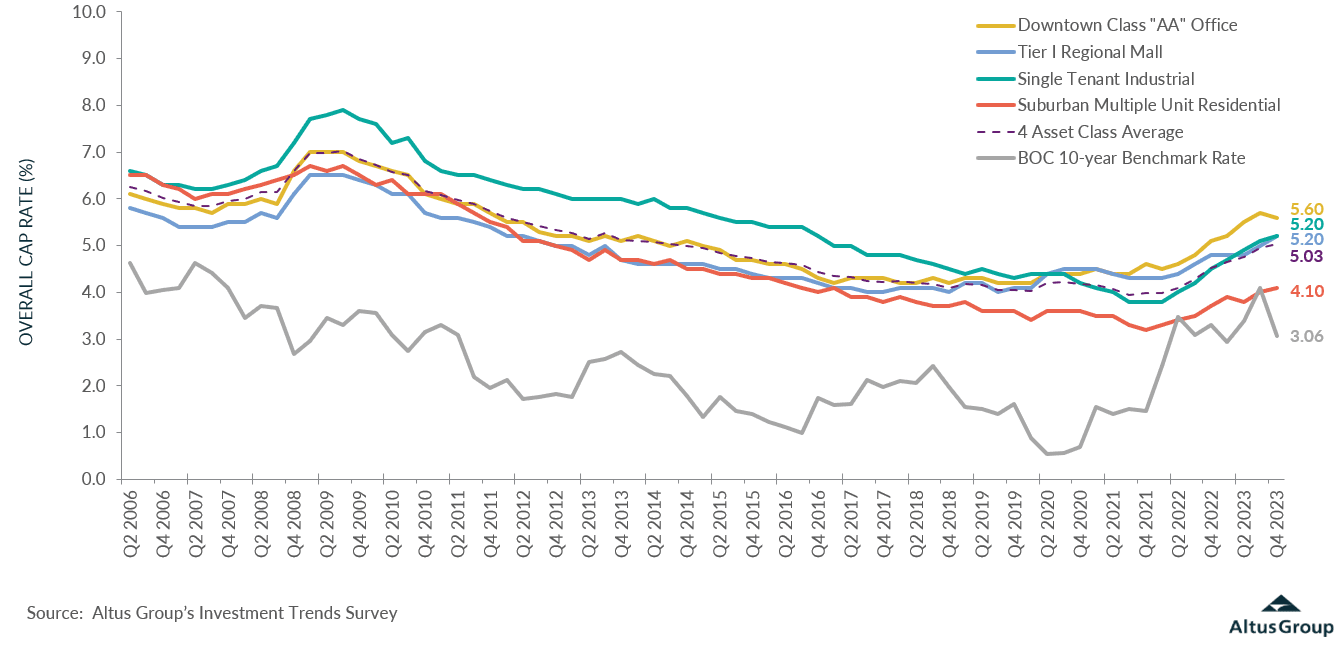

Figure 3 - GTA OCR trends across 4 benchmark asset classes

In 2023, higher interest rates and inflationary pressures slowed investment activity across all major markets in Canada as most investors adopted a “wait-and-see” approach. Despite the economic slowdown, the GTA market remained one of the top three preferred Canadian markets among investors, as the industrial sector contributed to over one-third of the GTA’s annual investment volume and matched the total investment volume recorded in 2022. Moreover, investors have maintained a positive outlook with the anticipation of lower interest rates in the second half of 2024, and a market supported by strong underlying demographic and economic fundamentals.

Authors

Jennifer Nhieu

Senior Research Analyst

Wyland Milborne

Market Analyst

Authors

Jennifer Nhieu

Senior Research Analyst

Wyland Milborne

Market Analyst

Resources

Latest insights