The 21st Century ROAD to Housing Act: What CRE professionals need to know

The 21st Century ROAD to Housing Act has passed: Learn about key opportunities, risks, and the Treasury rulemaking CRE professionals may want to track.

The 21st Century ROAD to Housing Act: What CRE professionals need to know

The 21st Century ROAD to Housing Act has passed: Learn about key opportunities, risks, and the Treasury rulemaking CRE professionals may want to track.

Author

Cole Perry

Associate Director of Research, Altus Group

Key highlights

21st Century ROAD to Housing Act (H.R. 6644) passed both chambers but has not yet been signed; the President has conditioned his signature on unrelated legislation; if enacted, it will be the most significant federal housing legislation in roughly 30 years: primarily a supply-side package targeting the scarcity at the root of the affordability crisis

On the financing side, updated FHA multifamily loan limits and expanded bank community investment capacity lower the cost of building and lending into development; a separate demand-side pilot targets sub-$100K mortgage access for underserved buyers

Senate drafting caught BTR in the crossfire of the institutional investor ban; after industry outcry and bipartisan pressure, both the BTR ban and a subsequent forced-sale requirement were stripped

The institutional investor ban, barring certain entities from owning more than 350 single-family homes, remains in the final bill and is arguably its most contested provision; how Treasury defines ownership thresholds will determine how much friction it creates for CRE platforms with single-family exposure

What the 21st Century ROAD to Housing Act does

The legislation merges two parallel congressional efforts, the Senate’s ROAD to Housing Act and the House’s Housing for the 21st Century Act, into a supply-side reform package spanning 12 titles and more than 50 sections. The Senate passed a combined version in March 2026, the House passed its amended version in May, and both chambers reached final agreement in late June with broad bipartisan support. Key provisions include:

National Environmental Policy Act (NEPA) streamlining: Expanded categorical exclusions from environmental review for Department of Housing and Urban Development (HUD)-assisted infill projects and office-to-residential conversions

Innovation Fund: $200M/year competitive grants rewarding cities that demonstrate measurable housing supply growth

RESIDE Act: $1M-$10M grants to convert vacant warehouses, factories, malls, and hotels into housing

Federal Housing Administration (FHA) loan limit updates: Multifamily limits adjusted to reflect current construction costs, with the indexing formula reformed

Zoning reform guidance: Non-binding HUD best practices nudging localities toward reduced parking minimums, higher floor area ratio (FAR), and accessory dwelling unit (ADU) allowances

Build Now Act: Adjusts Community Development Block Grant (CDBG) formula allocations up or down based on whether a city's housing supply is actually growing

Manufactured and modular housing reforms: Expanded definition of manufactured homes (eliminating the permanent-chassis requirement); review and streamlining of FHA construction financing for modular homes

Small-dollar mortgage access: FHA pilot program and lender incentives for sub-$100K mortgages

The negotiation

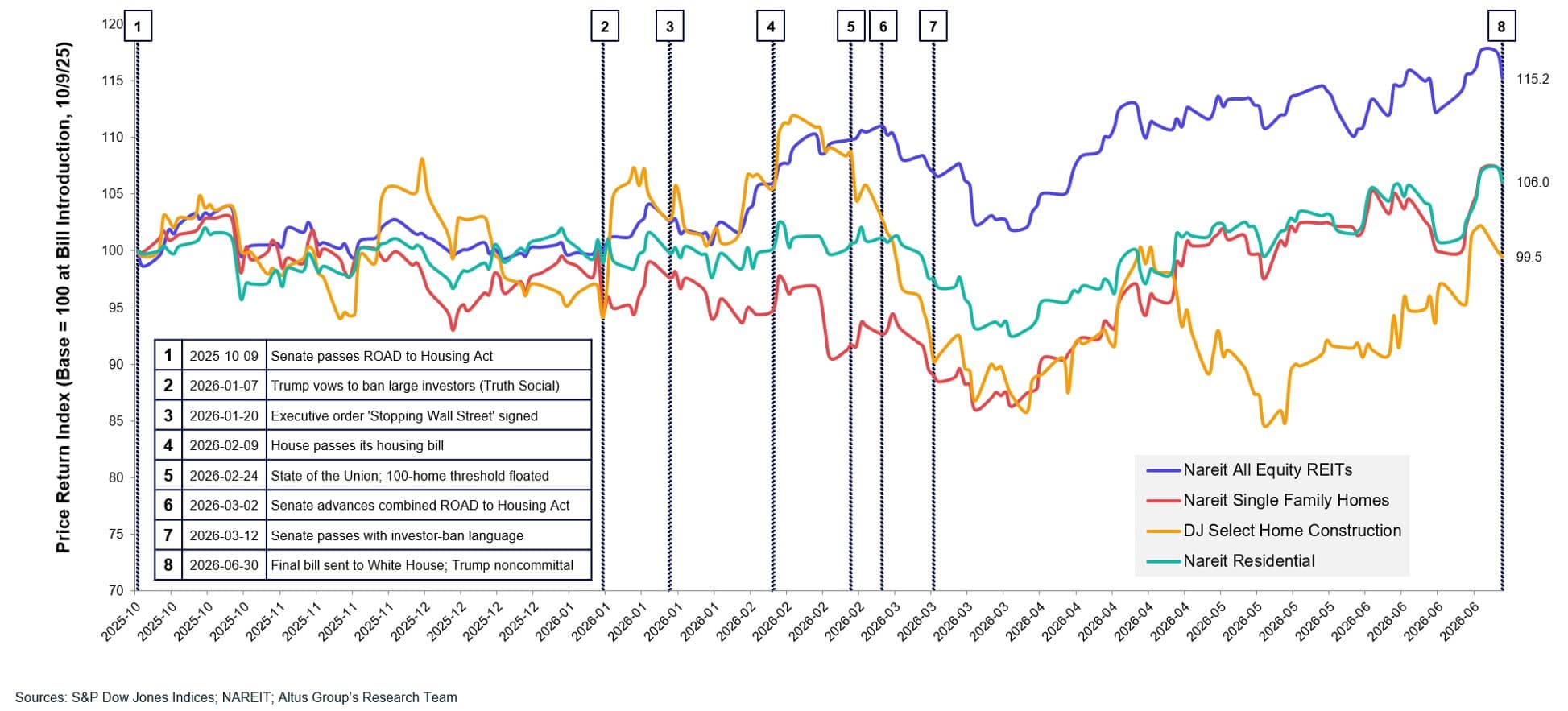

Figure 1: Real-estate indices vs. policy milestones (indexed to 100)

In January 2026, President Trump signed an Executive Order directing agencies to restrict institutional investor acquisitions of existing single-family homes, with a clean carve-out for build-to-rent (BTR). The Order also directed Treasury to develop the relevant definitions, setting up its current rulemaking authority. Congress needed to turn that policy into a permanent federal law that no future president could undo with a pen stroke. What nearly derailed the effort was how the Senate drafted it.

BTR caught in the crossfire (and eventually freed)

The Senate’s version defined “purchase” broadly enough to capture new construction, inadvertently banning BTR alongside single-family rental (SFR) acquisitions. A revised version added a BTR exemption but attached a seven-year forced-sale requirement, making new BTR development economically unviable in virtually any case. Analyses from the Pew Charitable Trusts, the Urban Institute, and the Terner Center at UC Berkeley projected losses of up to 100,000 new units annually; the National Association of Home Builders (NAHB) withdrew support and a bipartisan group of 76 House members called it a provision that would halt BTR production nationwide. The final bill strips both, leaving a straightforward BTR exemption and the SFR acquisition ban that the Executive Order originally envisioned.

What remains: the institutional investor ban (Title X, still contested)

The final bill prohibits any entity controlling 350 or more single-family homes from acquiring additional existing SFRs, with penalties of up to $1M per violation or three times the purchase price, whichever is greater. The ban is prospective (no forced divestiture of existing portfolios) and sunsets 15 years after its effective date. Notably, Congress framed the provision in its own text as a supply measure, stating the section is intended to expand the number of single-family homes available to individuals for purchase. Critics nonetheless argue it sits in tension with the other titles designed to unlock private investment in housing, and that the line between "institutional investor" and "large landlord" is harder to draw than the headline restriction suggests. How Treasury defines ownership thresholds across fund structures and joint ventures will determine how much friction this provision ultimately creates.

CRE: Opportunities and risks from the 21st Century ROAD to Housing Act

With the final bill’s shape now set, here is what it means in practice.

Opportunities

Distressed asset repositioning: A core provision to H.R. 6644, the RESIDE Act, creates a federally supported pathway for converting vacant retail, hotel, and industrial assets into attainable housing, while the NEPA categorical exclusion separately eases office-to-residential conversions.

Expanded bank capital: The Community Investment and Prosperity Act raises the cap on bank public welfare investments from 15% to 20%, broadening the lending pool for community development and mixed-use projects.

Zoning and density tailwinds: HUD's non-binding guidance builds federal momentum behind parking, setback, and FAR reforms that improve mixed-use development economics.

Opportunity Zone (OZ) stacking: HUD competitive grants now give additional weight to projects in qualified OZs, potentially layering favorably with existing OZ tax incentives.

Risks

Regulatory uncertainty: The investor ban creates compliance complexity for any CRE platform with single-family residential adjacency; portfolio aggregation, JV structures, and fund-level ownership will require careful legal review, particularly given the statute's broad "direct or indirect investment control" test.

Affordability strings on conversions: The RESIDE Act defines attainable housing as serving households at or below 120% of area median income (AMI), with a majority of units affordable at or below 60% AMI, limiting its usefulness for market-rate repositioning.

Unfunded mandates: Programs like the RESIDE act and the Innovation Fund carry their own explicit authorizations (e.g., $200M/year for the Innovation Fund through FY2031), but authorization is not funding. Their real-world impact depends on future appropriations cycles.

What to watch

The bill puts a number of new tools in the hands of developers and municipalities: conversion grants and NEPA exclusions for repositioning distressed assets, supply-growth incentives through the Innovation Fund and Build Now Act, expanded bank investment capacity, pattern-book and pre-review programs to speed construction, and federal zoning guidance to lean on locally. Most of this is upside for the development pipeline, though much of it depends on future appropriations to materialize.

The institutional investor ban on additional single-family acquisition is the provision to watch most closely. Its practical reach depends on how Treasury defines "investment control" across fund structures and joint ventures, and the BTR drafting episode demonstrated how much that line-drawing matters. CRE platforms with single-family exposure should track the Treasury rulemaking carefully, since that is where the ban's ultimate scope will be set.

Note: H.R. 6644 passed both the House and Senate and was presented to the President on June 29, 2026. It is not yet law. All provisions described are subject to change until enacted.

Boost investor confidence with independently managed valuations

Independent appraisals trusted by funds, investors, lenders, and public entities around the world.

Want to be notified of our new and relevant CRE content, articles and events?

Disclaimer

This publication has been prepared for general guidance on matters of interest only and does not constitute professional advice or services of Altus Group, its affiliates and its related entities (collectively “Altus Group”). You should not act upon the information contained in this publication without obtaining specific professional advice.

A number of factors may influence the performance of the commercial real estate market, including regulatory conditions and economic factors such as interest rate fluctuations, inflation, changing investor sentiment, and shifts in tenant demand or occupancy trends. We strongly recommend that you consult with a qualified professional to assess how these and other market dynamics may impact your investment strategy, underwriting assumptions, asset valuations, and overall portfolio performance.

No representation or warranty (express or implied) is given as to the accuracy, completeness or reliability of the information contained in this publication, or the suitability of the information for a particular purpose. To the extent permitted by law, Altus Group does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. The distribution of this publication to you does not create, extend or revive a client relationship between Altus Group and you or any other person or entity. This publication, or any part thereof, may not be reproduced or distributed in any form for any purpose without the express written consent of Altus Group.

Author

Cole Perry

Associate Director of Research, Altus Group

Resources

Latest insights