Calgary commercial real estate market update – Q4 2025

While the 2025 total transaction volume demonstrated resilience, the market operated under a different set of pressures compared to 2024’s record-breaking activity.

Key highlights:

Source: Altus Data Studio market data and analysis

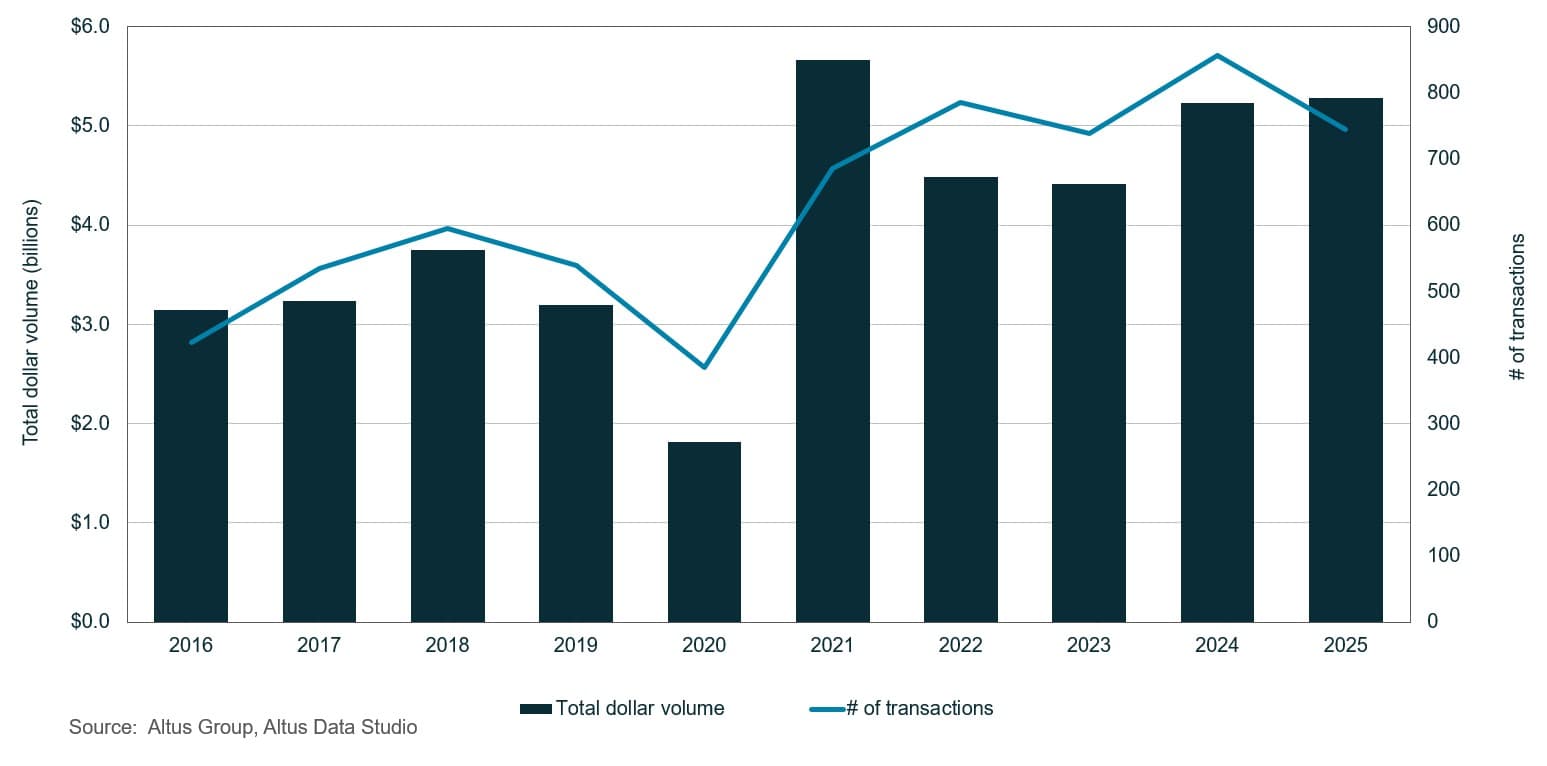

By the final quarter, Calgary reported a nominal increase in investment activity, with nearly $5.3 billion in dollar volume transacted, a 1% increase year-over-year

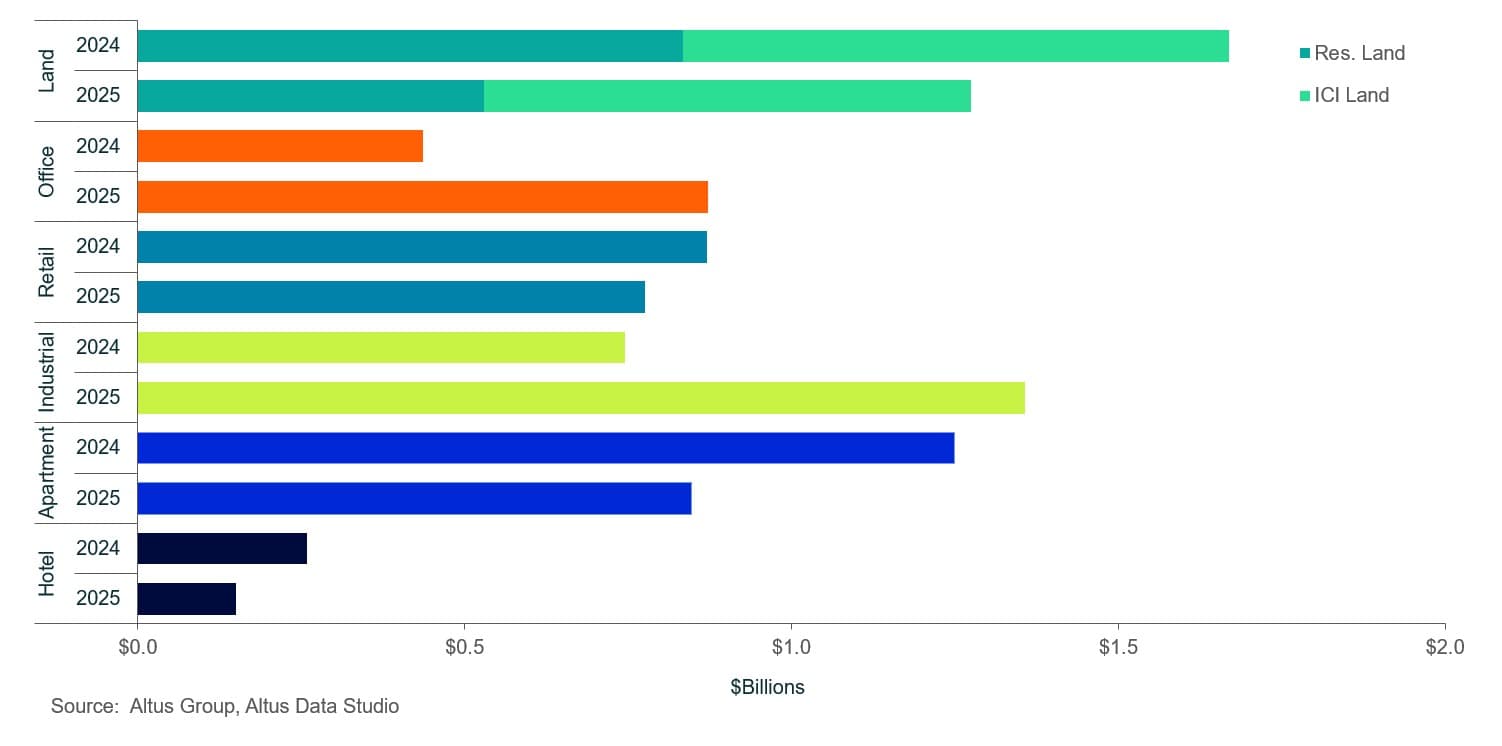

The office sector saw a positive momentum in leasing activity, with $872 million in dollar volume transacted, representing a significant 100% increase year-over-year

The industrial sector recorded nearly $1.4 billion in dollar volume transacted, a substantial 82% increase year-over-year

The retail sector reported an 11% decrease year-over-year, with $776 million in dollar volume transacted, as a lack of available inventory constrained investment activity

Despite the 32% year-over-year decrease, the multi-family sector remained robust by historical standards, with $848 million in dollar volume transacted, supported by strong demographic fundamentals

The land sector recorded $1.3 billion in dollar volume transacted, down 24% year-over-year.

The residential land sub-sector recorded $530 million in dollar volume transacted, while the ICI land sub-sector recorded $745 million, down 36% and 11% year-over-year, respectively

In the final quarter of 2025, Calgary saw an increase in commercial investment, marking a marginal 1% increase year-over-year

According to an analysis of transactions based on Altus Data Studio data, by the final quarter of 2025, Calgary’s commercial real estate market recorded a total investment volume of nearly $5.3 billion, a marginal 1% year-over-year increase (Figure 1). While activity remained steady throughout the first three quarters, momentum accelerated significantly in the final period as capital began to move more freely following a phase of mid-year caution.

Figure 1: Calgary property transactions - All sectors by year

Despite this stability, Calgary was notably overtaken by Edmonton in growth rate. This shift was largely driven by Edmonton’s aggressive expansion in industrial logistics and a surge in retail investment, as institutional capital sought higher yields in more affordable secondary markets.

Alberta’s evolution as a Western “affordability engine” provided a necessary counterweight to the economic stagnation observed in Canada’s eastern provinces. While Ontario and British Columbia faced headwinds from prohibitive housing costs, Calgary benefitted from several years of sustained interprovincial migration and a proactive municipal environment. These demographic and regulatory advantages reinforced the city’s position as a premier destination for defensive investment strategies amidst a volatile national landscape.

Macroeconomic drivers and geopolitical considerations

This stability of Calgary’s broader market was further reinforced by the legal protections of the Canada-United States-Mexico Agreement (CUSMA). For Calgary, these protections effectively insulated regional investments, particularly within the energy and emerging tech sectors, from the volatility of U.S. trade protectionism. Although market sentiment remained tempered by the upcoming 2026 mandatory review of CUSMA, Calgary’s core fundamentals remained attractive to participants who had already priced in these geopolitical uncertainties by year-end.

Significant shifts in monetary policy and national economic indicators also shaped the investment climate. On December 10, 2025, the Bank of Canada (BoC) elected to maintain the overnight rate at 2.25% following two consecutive reductions, providing a critical window of stability for Calgary’s capital markets following mid-year volatility. Statistics Canada reported that real gross domestic product (GDP) contracted at an annualized rate of 0.6% (a 0.2% quarterly decline) in the fourth quarter, driven by a reduction in business inventories. Calgary’s local economy remained bolstered by sustained household spending from a growing interprovincial migrant population, which helped mitigate the impact of the national slowdown.

Calgary’s labour market also showed notable improvement toward the end of the year. The local unemployment rate dropped to 6.8% in December, down from 7.8% in December 2024. While the national unemployment rate rose to 6.8%, Calgary’s downward trend signalled a tightening local market and absorption of new workforce participants. Despite the finalized national GDP growth at 1.7%, the slowest pace of expansion since 2020, Calgary’s improving job market and relative demand for industrial and professional services established a stable, albeit conservative, baseline for commercial underwriting entering 2026.

Calgary retail investment activity

By the end of 2025, Calgary’s retail sector recorded a total transaction volume of $776 million. This figure represented an 11% decrease year-over-year, though market analysis indicated that this contraction was not a symptom of waning investor appetite. Rather, the decline was primarily attributed to a persistent scarcity of high-quality, available inventory. Owners of top-tier assets largely opted to retain their holdings throughout the year, buoyed by the perceived stability and consistent performance of the sector despite broader macroeconomic volatility.

A defining retail trend of 2025 was the sustained demand for neighbourhood food-anchored retail and shopping centres with integrated redevelopment potential. These assets remained highly sought-after due to their defensive nature and stable cash flows. However, the combination of elevated financing constraints and persistent economic uncertainty severely restricted new deliveries. This supply-side shortage intensified competition for existing assets, as investors prioritized “inflation-resistant” retail formats that catered to the daily needs of Calgary’s growing population.

As the city’s population surged, particularly within the northern corridors and deep southern districts, the strategic focus for developers and institutional property owners shifted toward recapitalization and diversification of aging retail footprints. This trend was exemplified by significant initiatives at major hubs such as Midtown Station (adjacent to Chinook Centre), Glenmore Landing, Northland Village Mall, Stadium Shopping Centre and Deerfoot City.

The prevailing investment strategy involved the integration of multi-residential towers directly into existing shopping centre sites. By converting underutilized traditional parking surfaces into high-density residential units, firms successfully bolstered asset valuations while securing a captive consumer base. This “mixed-use” evolution became a cornerstone of risk mitigation in 2025, as it allowed owners to maximize land value within a market characterized by a constrained supply of new commercial space and high barrier-to-entry costs.

Calgary industrial investment activity

The Calgary industrial sector maintained exceptional momentum throughout 2025, concluding the year with a total transaction volume that neared $1.4 billion. This figure represented a substantial 82% increase year-over-year, underscoring the city’s enduring appeal as a premier inland port and the primary strategic distribution hub for Western Canada. The robust demand for industrial space was further validated by market data from Altus Group’s Data Studio, indicating Calgary’s industrial availability rate decreased by 60 basis points (bps) over the twelve-month period, settling at 5.9% by the fourth quarter of 2025. This downward trajectory in availability created persistent upward pressure on net rental rates as the competition for functional logistics space intensified.

On the development front, the market saw the delivery of one new industrial building, totalling approximately 38,500 square feet. Although this specific asset remained fully available at the time of completion, it represented only a fraction of the broader activity within the sector. By year-end, the development pipeline remained robust, with 11 industrial buildings under construction. This inventory totalled nearly two million square feet, of which 41% remained available for lease, indicating a healthy level of pre-leasing activity for upcoming supply.

Despite the broader macroeconomic headwinds, Calgary continued to record a significant volume of speculative development. Developers maintained high levels of confidence in the market’s long-term fundamentals, particularly as the city’s role in the national supply chain continued to expand.

Calgary multi-family investment activity

The multi-family sector experienced a notable contraction in investment volume, with total transactions amounting to approximately $848 million. This figure represented a 32% decrease year-over-year, a slowdown that was largely attributed to the high base effect established during the record-breaking activity of 2024. Despite this drop in total dollar volume, investment activity remained consistent with long-term historical benchmarks. Calgary’s robust market fundamentals, specifically its comparatively lower entry costs and sustained demand for housing, continued to position the city as a resilient destination for institutional and private capital amidst a broader national cooling.

Investor confidence was sustained by Calgary’s unique position as a destination for interprovincial migration. Throughout the second half of 2025, capital was increasingly rebalanced toward Alberta as investors sought shelter from the economic stagnation observed in Ontario and British Columbia. The consistent influx of residents from other Canadian provinces provided a reliable “demand floor,” reinforcing the sector’s status as a defensive asset.

A significant driver of sentiment in 2025 was the shifts in the federal financing frameworks. The introduction of the CMHC MLI Select risk-based pricing model on July 14, 2025 acted as a catalyst for strategic acquisitions. By aligning investment goals with specific social outcomes, such as affordability and energy efficiency, investors were able to access preferential borrowing rates and extended amortizations. This environment fostered a “flight-to-quality” and a strategic pivot toward high-density assets in the downtown core. Rather than exiting the market due to interest rate volatility, sophisticated investors utilized these government-backed programs to mitigate risk, securing long-term operational stability while addressing national affordability challenges through denser, more efficient asset profiles.

Calgary office investment activity

Calgary’s office sector recorded a substantial 100% year-over-year increase in investment volume, with nearly $872 million in dollar volume transacted. A pronounced bifurcation between office classes largely defined this surge in activity, as investors and tenants alike prioritized high-quality, amenity-rich environments. This “flight-to-quality phenomenon was reflected in leasing data, with Class A transactions involving 77 deals and totalling nearly 2.9 million square feet. In contrast, Class B and C assets experienced significantly less liquidity, accounting for only 25 transactions and approximately 443,000 square feet, highlighting the growing functional obsolescence of buildings that failed to meet modern corporate standards.

The downtown availability rate reached 23.7% in the fourth quarter, a 40-bps contraction year-over-year, primarily due to continued rightsizing efforts in the downtown core. However, availability in the suburban and Beltline submarkets tightened, supported by diverse tenant demand in healthcare and education. A crucial factor in market stabilization was the City of Calgary’s Downtown Development Incentive program and the Housing Accelerator Fund. By November 2025, 21 office-to-residential conversion projects were approved, scheduled to remove 2.68 million square feet of underutilized office space from the inventory and transition it into over 2,600 residential units.

By the year-end, Calgary’s office availability experienced a sharp correction, settling at 19.8%, a 210 bps decrease year-over-year. This improvement was sustained by disciplined supply-side management, with no new office completions recorded in the fourth quarter. The construction of the Westwind Business Campus III remained on hold. Consequently, the year concluded with a movement toward a healthier equilibrium, as property owners prioritized capital improvements to maintain the competitiveness of Class A assets.

Calgary land investment activity

Investment activity in the land sector, encompassing both the residential land and ICI land sub-sectors, experienced a contraction by the fourth quarter. Total transaction volume reached nearly $1.3 billion for the year, representing a 24% decrease year-over-year. This downturn reflected a broader sense of caution among developers and investors as they navigated evolving federal immigration policies, shifting macroeconomic indicators and trade uncertainty.

The residential land sub-sector saw a pronounced 36% year-over-year decline to $530 million. This was primarily driven by temporary saturation in the multi-family market and a deceleration in international migration, which led developers to adopt a more conservative stance on initiating large-scale greenfield projects. Similarly, the ICI sector recorded approximately $745 million in transactions, representing an 11% decrease year-over-year. This continued moderation in capital deployment suggested that institutional and private investors were adopting a “wait-and-see” approach, prioritizing the build-out of existing pipelines over the acquisition of new development sites until market conditions demonstrated greater stability.

Figure 2: Calgary property transactions by asset class (Q4 2024 vs. Q4 2025)

Notable Calgary property transactions

The following are the notable transactions for the Q4 2025 Calgary commercial real estate market update:

505 Quarry Park Boulevard SE (Imperial Oil Campus) – Office

Imperial Oil Ltd. has finalized the sale of its 19.4-acre, custom-built headquarters campus in southeast Calgary’s Quarry Park to Dominium (Quarry) Corp., an affiliate of Calgary-based developer Dominium. Brokered by CBRE, the five-building, 698,583-square-foot complex closed at a purchase price of $60 million, or roughly $85.89 per square foot.

The transaction price represented a significant decline from the $416.8 million expended by Imperial Oil to acquire the property in 2016. This real estate divestment followed a severe corporate restructuring that led to a 20% workforce reduction at Imperial Oil’s Calgary operation. While the energy company has secured a short-term leaseback for a minor portion of the campus, local market experts projected a multi-year absorption period to fill the substantial remaining vacancy.

3023 16th Street SW (The Edward) – Apartment

Chartwell Retirement Residences has expanded its Western Canadian portfolio with the $53.1 million acquisition of The Edward, a premier luxury senior living community in Calgary. Located at 3023 16th Street SW, situated three kilometres from the downtown core and adjacent to the vibrant Marda Loop cultural hub, the boutique, five-story senior apartment complex was purchased for $53 million, representing approximately $559,000 per suite.

Originally developed by Section23 Developments and opened in 2021, the upscale facility featured 95 independent living suites with an 86% occupancy rate, a 5.5% capitalization rate, and monthly rents starting at $4,500 for studio apartments. Real estate firm Jones Lang LaSalle (JLL) represented the vendor in the transaction, highlighting the property’s premium positioning. This strategic acquisition underscored Chartwell's commitment to growing its footprint in Alberta’s robust and affluent retirement housing market.

10450 Macleod Trail SE (Toys R Us) – Retail

The sale of the Toys "R" Us property at 10450 Macleod Trail SE marked a notable transition in Calgary’s retail landscape. Following a strategic restructuring by parent company Putnam Investments, which included the closure of 13 Canadian locations since January 2025, the iconic 42,070-square-foot commercial building was placed on the Alberta real estate market with a listing price of $21 million.

Originally constructed in 1988, the 4.34-acre site occupied a prominent position along the high-traffic Macleod Trail corridor and was positioned as a premier, high-density redevelopment opportunity equipped with extensive parking. Real estate projections indicated that the former toy warehouse was poised to undergo a major transformation. Industry experts anticipated the site would either be completely redeveloped into a modern retail facility, subdivided into a multi-tenant configuration featuring additional commercial pad sites, or converted by a national sports and recreation brand.

4600 Crowchild Trail NW (Northland Professional Centre) – Retail & Office

Located in Calgary’s Northwest quadrant, 4600 Crowchild Trail NW comprised an established, five-storey suburban office building positioned directly adjacent to the Northland Village area. The property operated as a prominent hub for medical, dental and professional services, benefiting from high visibility along the Crowchild Trail corridor. At the time of sale, it maintained an 82% occupancy rate and a 9% capitalization rate.

In a transaction that included the Northland Village Shopping Centre, Primaris REIT closed the sale to GWL Realty Advisors (an affiliate of Toronto-based Canada Life Assurance) for a premium consideration of $154 million, which represented GWL’s largest retail acquisition in over five years.

Looking ahead to 2026 Calgary investment activity

2025 marked a pivotal transition for Calgary’s commercial real estate market. While the year-end total transaction volume demonstrated resilience, anchored by a robust industrial sector and sustained interest in Class AAA office assets, the market operated under a markedly different set of pressures compared to the preceding period of record-breaking activity. The cooling of the land sector, juxtaposed with the significant positive momentum of the office and industrial segments, underscores a broader structural shift toward defensive, high-quality and strategically diversified asset profiles.

Looking ahead to 2026, Calgary’s market fundamentals remain underpinned by its continued status as an “affordability engine” and its appeal as a primary inland logistics hub for Western Canada. The successful navigation of 2025’s “wait-and-see” environment suggests that the market has matured, shifting from speculative, growth-at-all-costs, momentum toward a disciplined focus on redevelopment, functional obsolescence removal and long-term risk mitigation.

As geopolitical variables such as the pending CUSMA review and national economic headwinds persist, investors will likely continue to prioritize assets that offer stable cash flows and integration with Calgary’s evolving demographic needs. While supply-side constraints in specific retail and industrial segments may continue to challenge immediate investment liquidity, the underlying demand signals, bolstered by a tightening labour market and strategic city-led development initiatives, point toward a stable, conservative and opportunity-rich landscape for participants ready to commit to Calgary’s long-term growth trajectory.

Leverage our real estate data and predictive analytics

The performance attribution, predictive analytics and market intelligence you need to explain performance and improve decision making.

Want to be notified of our new and relevant CRE content, articles and events?

Disclaimer

This publication has been prepared for general guidance on matters of interest only and does not constitute professional advice or services of Altus Group, its affiliates and its related entities (collectively “Altus Group”). You should not act upon the information contained in this publication without obtaining specific professional advice.

A number of factors may influence the performance of the commercial real estate market, including regulatory conditions and economic factors such as interest rate fluctuations, inflation, changing investor sentiment, and shifts in tenant demand or occupancy trends. We strongly recommend that you consult with a qualified professional to assess how these and other market dynamics may impact your investment strategy, underwriting assumptions, asset valuations, and overall portfolio performance.

No representation or warranty (express or implied) is given as to the accuracy, completeness or reliability of the information contained in this publication, or the suitability of the information for a particular purpose. To the extent permitted by law, Altus Group does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. The distribution of this publication to you does not create, extend or revive a client relationship between Altus Group and you or any other person or entity. This publication, or any part thereof, may not be reproduced or distributed in any form for any purpose without the express written consent of Altus Group.

Authors

Jennifer Nhieu

Senior Research Analyst

Nhu Pham

Market Analyst

Authors

Jennifer Nhieu

Senior Research Analyst

Nhu Pham

Market Analyst

Resources

Latest insights