US commercial real estate debt markets close 2025 on a stronger note

Explore how Q4 2025 brought lower benchmark rates, tighter spreads, and stronger lender competition to the commercial real estate financing market.

Key highlights:

All-in rates dropped significantly: Borrowers are finally seeing meaningful relief in their financing costs with the average quarter-over-quarter change in all-in debt costs across all property types down -45 basis points, and year-over-year declines averaging -66 bps

Term SOFR fell 69 bps year-over-year: Short-term benchmark rates continued their descent, with Term SOFR declining to 3.99% in Q4 2025, down 34 bps from the prior quarter and reflecting the Fed's ongoing policy normalization

Year-over-year, all product types posted spread compression: Lower-leverage floating-rate senior short products saw the most compression, with average spreads falling 33 bps (11%) to 253 bps over Term SOFR

Lender competition increased: Borrowers received an average of 5.2 competitive quotes for new financing, up from 5.1 in Q3 2025 and 4.7 from a year ago; with more lenders chasing deals, sponsors now have additional negotiating leverage

Office activity rebounded: Office's share of total quotes increased 4 percentage points quarter-over-quarter to 17%, suggesting lenders are selectively re-engaging with the sector after an extended pullback

Favorable winds for CRE borrowers as Q4 2025 closes

The fourth quarter of 2025 brought welcome news for commercial real estate borrowers. After navigating an extended period of elevated rates and cautious lending, the market showed clear signs of normalization. Benchmark rates declined across all tenors, spreads compressed, and lender competition intensified. The Federal Reserve's rate-cutting cycle that began in late 2024 continued to filter through the capital markets, creating more favorable financing conditions for quality deals. The quarterly Debt Capital Markets Survey (DCMS) captured these shifts with over 1,500 quotes from seasoned industry professionals, painting a picture of a market finding its footing heading into 2026.

Quote activity and market composition

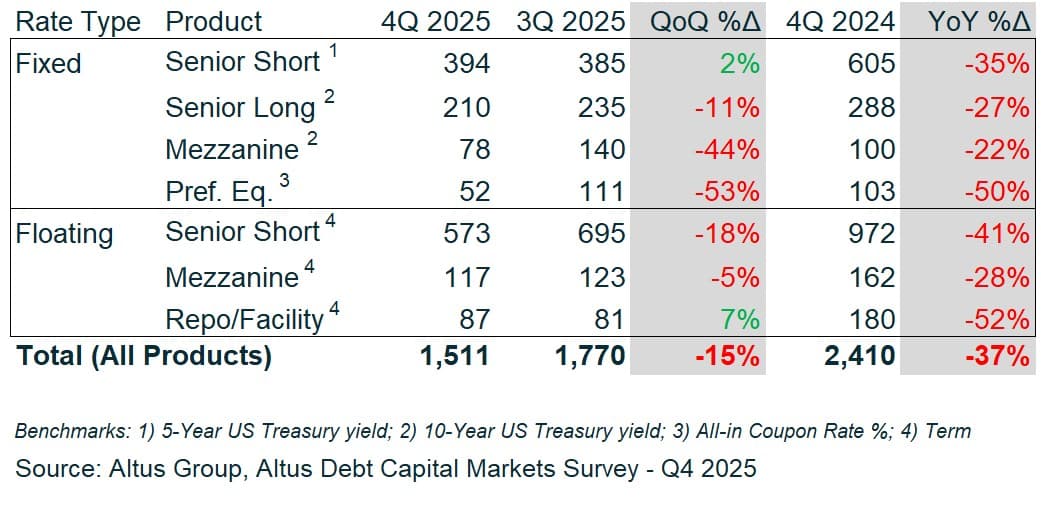

Total surveyed quotes came in at 1,511 for the quarter, down 15% from Q3 2025 and 37% from Q4 2024. The decline was largely seasonal. Holiday schedules and year-end vacation time kept some market participants on the sidelines. Despite the lower volume, the average number of quotes per survey participant actually ticked up to 13.3 from 12.7, indicating engaged lenders remained active.

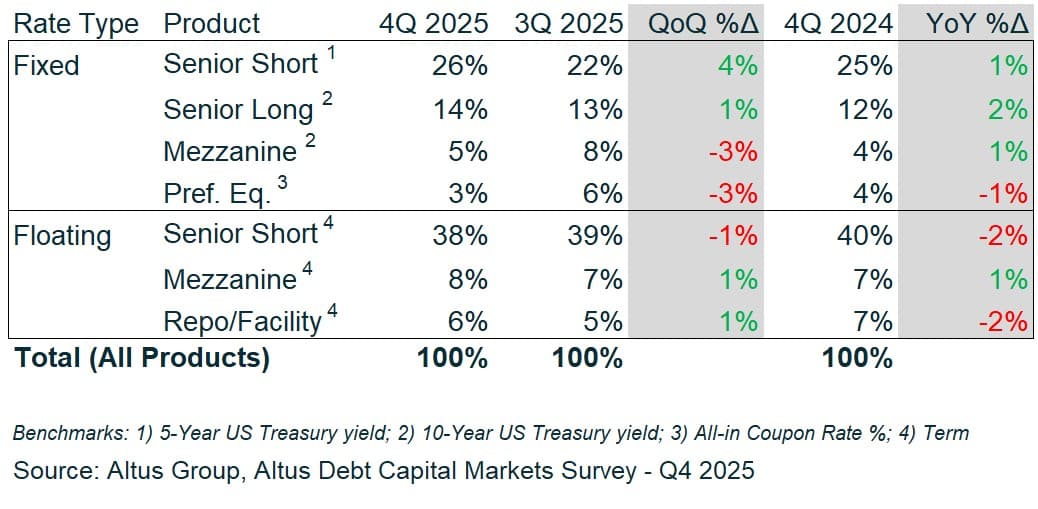

The product mix shifted modestly toward fixed-rate offerings. Fixed-rate products represented 49% of total quotes, with fixed-rate senior short seeing its share rise to 26% from 22% the prior quarter. Floating-rate senior short products remained the single largest category at 38%, but slipped slightly from 39%. This shift may reflect borrowers locking in rates amid expectations of further Fed easing, or simply the natural ebb of near-term refinancing needs.

Figure 1: Surveyed quotes - Count of quotes received by product type

Figure 2: Product mix - As a percentage of total quotes received

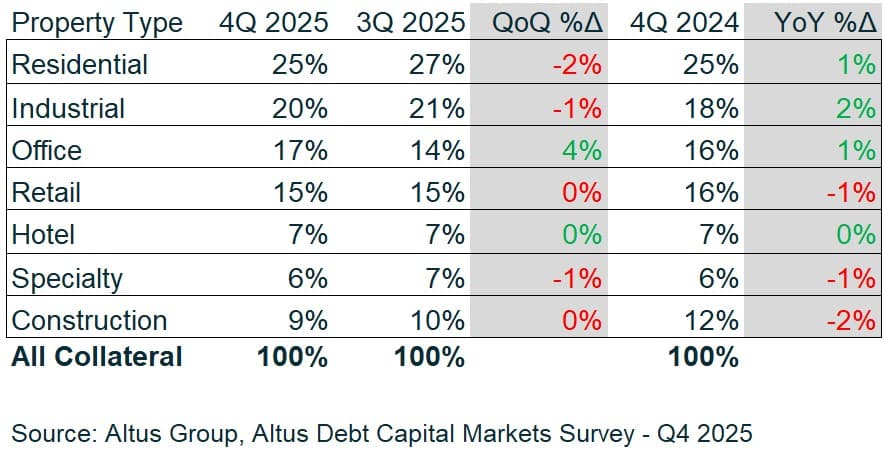

On the collateral side, residential held its top position at 25% of quotes, followed by industrial at 20%, and office at 17%. The notable story here is office. After years of being out of favor, office saw its share jump 4 percentage points quarter-over-quarter. Lenders appear to be differentiating more thoughtfully within the sector, finding opportunities in trophy assets and well-leased properties while steering clear of commodity products facing structural headwinds.

Figure 3: Collateral sector mix – As a percentage of total quotes received

Boost investor confidence with independently managed valuations

Independent appraisals trusted by funds, investors, lenders, and public entities around the world.

Benchmark rates: The yield curve normalizes

Benchmark yields continued their downward trajectory as the Fed's monetary policy normalization worked through the system. Term SOFR fell 34 bps quarter-over-quarter to a 3.99% average, while the 5-Year Treasury declined 13 bps to 3.67% and the 10-Year dropped 16 bps to 4.10%.

Year-over-year moves were even more dramatic. Term SOFR is down 69 bps from Q4 2024, the 5-Year is down 45 bps, and the 10-Year is down 18 bps. The yield curve, which had been sharply inverted for much of 2024, has flattened considerably. Short-term rates fell faster than long-term rates, a pattern typical of Fed easing cycles. For borrowers, this translates to meaningfully lower all-in costs, particularly on floating-rate debt.

Spreads: Compression across the board

Spreads tightened across most product types and collateral sectors in Q4 2025. The standout was lower-leverage floating-rate senior short financing, where average spreads fell to 253 bps, down 33 bps (11%) from 286 bps in Q3. Fixed-rate senior short products also saw compression, as did fixed-rate mezzanine and preferred equity.

Not everything tightened. Floating-rate mezzanine spreads widened to 780 bps over Term SOFR, up 40 bps (5%) from the prior quarter. Mezzanine lenders may be maintaining discipline on pricing even as senior debt becomes more competitive, or they could be responding to changing risk profiles in certain deal types.

Figure 4: Average spread by product type

By collateral type, retail and specialty assets saw the most spread compression for senior-short financing. Hotel was the outlier, with spreads widening 13% quarter-over-quarter to 379 bps. Construction spreads fell 15% to 357 bps, a welcome sign for a sector that has faced financing headwinds since the regional bank turmoil of 2023.

Figure 5: Senior-short spreads – Average spreads by select collateral type

All-in rates: Meaningful relief for borrowers

When you combine lower benchmarks with tighter spreads, borrowers win. All-in rates declined across most property types in Q4 2025. Residential fell to 537 bps (from 567 bps YoY), industrial to 543 bps (from 575 bps), and office to 609 bps (from 646 bps). Construction all-in rates reached 630 bps, down from 665 bps a year ago.

Across all property types and subtypes, the average quarter-over-quarter change in all-in rates was -45 bps, and the average year-over-year change was -66 bps. Only two collateral subtypes bucked the trend: Hotel Full Service and Retail Mall, both of which saw modest increases of 12-13 bps (about 2%) quarter-over-quarter. The rest of the market moved decisively lower.

Looking ahead

The Q4 2025 survey data tells a consistent story: conditions are improving. Lower benchmark rates, tighter spreads, and increased lender competition are making financing more accessible and less expensive. The resurgence of activity in office suggests capital is becoming more discerning rather than simply avoiding entire asset classes. Many questions remain around whether benchmark yields and spreads will stay range-bound as markets digest shifts in geopolitical, trade, and fiscal policy - alongside changing investor risk appetite. What is clear, however, is that as 2026 begins, CRE borrowers face a more favorable environment than they have seen in several years.

About the survey

The Debt Capital Markets Survey gathers insights into the CRE debt market from a select group of industry participants. Survey responses reflect the view of individual CRE professionals and are not assumed to reflect any firm or company view.

Participate in our future surveys on the debt capital market

Want to be notified of our new and relevant CRE content, articles and events?

Disclaimer

This publication has been prepared for general guidance on matters of interest only and does not constitute professional advice or services of Altus Group, its affiliates and its related entities (collectively “Altus Group”). You should not act upon the information contained in this publication without obtaining specific professional advice.

A number of factors may influence the performance of the commercial real estate market, including regulatory conditions and economic factors such as interest rate fluctuations, inflation, changing investor sentiment, and shifts in tenant demand or occupancy trends. We strongly recommend that you consult with a qualified professional to assess how these and other market dynamics may impact your investment strategy, underwriting assumptions, asset valuations, and overall portfolio performance.

No representation or warranty (express or implied) is given as to the accuracy, completeness or reliability of the information contained in this publication, or the suitability of the information for a particular purpose. To the extent permitted by law, Altus Group does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. The distribution of this publication to you does not create, extend or revive a client relationship between Altus Group and you or any other person or entity. This publication, or any part thereof, may not be reproduced or distributed in any form for any purpose without the express written consent of Altus Group.

Authors

Omar Eltorai

Senior Director of Research, Altus Group

Andrew Pabon

Director Global Advisory

Authors

Omar Eltorai

Senior Director of Research, Altus Group

Andrew Pabon

Director Global Advisory

Resources

Latest insights

Mar 12, 2026

CRE valuation has outgrown traditional processes: Is it time for a new approach?