CRE This Week: What's impacting the Canadian market

April 8, 2026 - Canada commercial real estate market insights, indicators, and notable transactions

April 8, 2026

Welcome to the latest edition of CRE This Week, curated by Altus Group’s Canada research team.

Our team has handpicked new and noteworthy market indicators, articles, and significant industry transactions that are impacting Canada's commercial real estate sector. We understand that your time is valuable, so we're excited to deliver research that helps you stay informed and saves you some time each Wednesday morning.

FEATURED TrANSACTIONS

Canada property transactions

Greater Toronto Area: Industrial

6780 Columbus Road, Mississauga

$11,800,000

$378 per sq. ft.

Brokers: Jason Vance & Kevin Brennan (CDNGLOBAL Indusite Realty), Ilan Friedner (Real Broker Ontario Ltd.)

Greater Vancouver Area: Industrial

5085 North Fraser Way, Burnaby

$53,274,435

$525 per sq. ft

Brokers: Lee Blanchard, Sean Ungemach, Nathan Kewin, Blake Gozda, Jeevan Bath (Cushman & Wakefield)

Greater Ottawa Area: Office

275 Bay Street, Ottawa

$2,750,000

$299 per sq. ft.

Brokers: Ronaldo Sayah (The Reps Brokerage) & Rami Bastawros (Royal LePage Performance Realty)

Greater Edmonton Area: Apartment

8710 91st Street NW, Edmonton

$3,400,000

$170,000 per unit

Greater Toronto Area

Sector | Municipality | Address | Price | Unit Price | Parameters | Brokers |

|---|---|---|---|---|---|---|

Industrial | Brampton | 40 & 44 West Drive | $15,750,000 | $598 | per sq. ft. | David Hoffman & George Siotas (Colliers), Ramandeep Gill (Gillfort Realty) |

Industrial | Vaughan | 177 Zenway Boulevard | $14,775,000 | $383 | per sq. ft. | |

Industrial | Scarborough | 90 Production Drive | $12,000,000 | $216 | per sq. ft. | Bryan Li, Ryan McDonnell, Jenny Fang (Jones Lang LaSalle) |

Greater Vancouver Area

Sector | Municipality | Address | Price | Unit Price | Parameters | Brokers |

|---|---|---|---|---|---|---|

Apartment | Vancouver | 2250 York Avenue | $5,995,000 | $428,214 | per unit | Chris Hayne, Billy Yang (Royal LePage Commercial) |

Retail | Abbotsford | 2455 West Railway Street | $4,500,000 | $776 | per sq. ft. | |

Industrial | Abbotsford | 30451 Great Northern Avenue, #110 | $2,550,000 | $499 | per sq. ft. |

Greater Ottawa Area

Sector | Municipality | Address | Price | Unit Price | Parameters | Brokers |

|---|---|---|---|---|---|---|

Retail | Ottawa | 1095 Carling Avenue | $49,000,000 | $273 | per sq. ft. | Matthew Johnson, Michael Pyman, Jordan Lovett, Jaiveer Kaberwal (Colliers) |

Apartment | Ottawa | 333 Metcalfe Street | $7,500,000 | $258,621 | per unit | |

Office | Nepean | 31 Auriga Drive | $6,600,000 | $225 | per sq. ft. |

Greater Edmonton Area

Sector | Municipality | Address | Price | Unit Price | Parameters | Brokers |

|---|---|---|---|---|---|---|

Apartment | Edmonton | 12040 82nd Street NW | $2,088,000 | $116,000 | per unit | |

Industrial | Edmonton | 7620 Yellowhead Trail NW | $1,950,000 | $171 | per sq. ft. | Colin Ewanchyshyn & Craig Hummel (Remax Commercial) |

Industrial | Edmonton | 12830 126th Avenue NW | $1,275,000 | $102 | per sq. ft. |

ECONOMIC PRINT

Canada commercial real estate market indicators

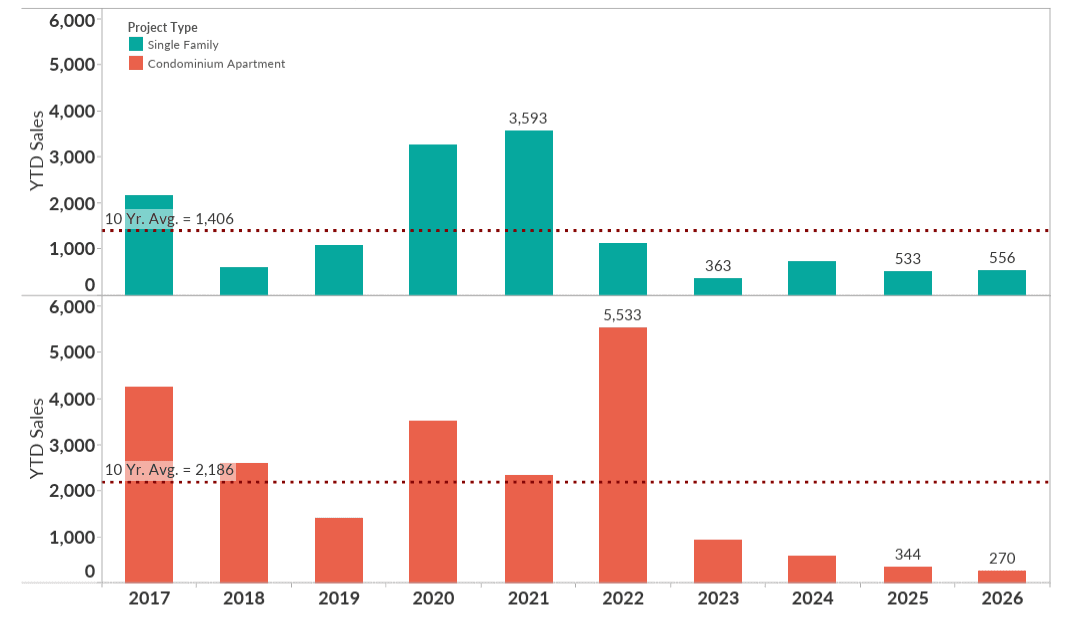

Year-to-date new home sales in the Greater Toronto Area

Through February, 826 new homes have been sold in the GTA: 556 single-family (up 4% YoY, but 60% below the 10-year average) and 270 condo apartments (down 22% YoY, 88% below the 10-year average). Inventory sits at 20,291 units, a 27-month supply.

According to Altus Research Manager Edward Jegg, cited in the latest BILD report, affordability concerns and geopolitical uncertainty are keeping buyers on the sidelines despite favourable rate conditions and near-decade-low pricing. Click here to read the full BILD New Homes Report for Febuary 2026.

Figure 1: Greater Toronto Area new home sales, year-to-date (2017 to 2026)

INSIGHTS Spotlight

Catch the latest research and insights from Altus

Why scenario analysis for CRE modeling needs new infrastructure

Persistent volatility across capital markets, leasing conditions, and operating costs has made rigorous scenario analysis a necessity, not just a best practice.

Webinar - Multifamily modeling and underwriting: A smarter approach built for scale

Thursday, April 9th | 1:00PM ET

Join us to see how our purpose-built multifamily cashflow modeling tool removes friction from analysis and underwriting, so you can move faster and make better-informed decisions.

About our research team

Edward Jegg

Research Manager, Data Solutions

Altus Group

Edward Jegg serves as a Research Manager on the Data Solutions team at Altus Group, leveraging over 35 years of extensive experience in the commercial real estate sector to deliver market intelligence to the industry. Jegg plays a key role in creating and disseminating detailed market reports across Canada, providing stakeholders with timely insights for investment decision-making. Jegg is a recognized expert, frequently offering media commentary on real estate trends and recently receiving the prestigious Chair's Award of Merit from BILD for his outstanding contribution to the field.

Jennifer Nhieu

Senior Research Analyst, Data Solutions

Altus Group

Jennifer Nhieu is a Senior Research Analyst, Data Solutions with Altus Group, where she specializes in providing timely, data-driven insights into the Canadian market. Leveraging her background in commercial real estate and geographic information science, Jennifer is a key contributor to Altus Group’s quarterly research insights. She transforms complex data sets into clear, actionable intelligence, helping stakeholders make informed decisions.

About the Data Solutions team

Behind every update in our newsletter is the work of our Data Solutions team, a group dedicated to keeping you informed on commercial real estate activity across Canada. From Vancouver to Toronto (and everywhere in between), they track transactions, visit properties, and add the local context that numbers alone can’t capture. Their work goes beyond deals, by providing insights into new home developments and sales trends, as well as detailed office and industrial inventory data across key markets, from Montreal and Calgary to Winnipeg, Quebec City, and Atlantic Canada.

Disclaimer: The opinions expressed in this newsletter are solely those of the authors and are not endorsed by Altus Group Limited, its affiliates and its related entities (collectively “Altus Group”). This publication has been prepared for general guidance on matters of interest only and does not constitute professional advice or services of Altus Group. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy, completeness or reliability of the information contained in this publication, or the suitability of the information for a particular purpose. To the extent permitted by law, Altus Group does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. The distribution of this publication to you does not create, extend or revive a client relationship between Altus Group and you or any other person or entity. This publication, or any part thereof, may not be reproduced or distributed in any form for any purpose without the express written consent of Altus Group.

Resources

Latest insights